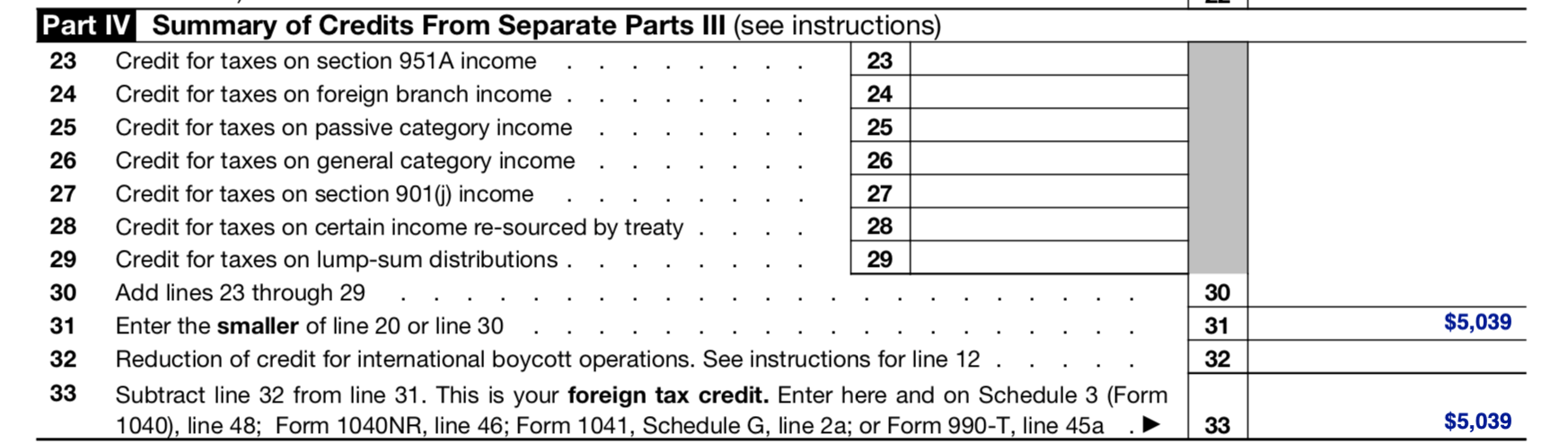

901(j) Income

Evaluating Income Tax Revenue Elasticities Economic Journal Royal Economic Society vol. C Tested income groups.

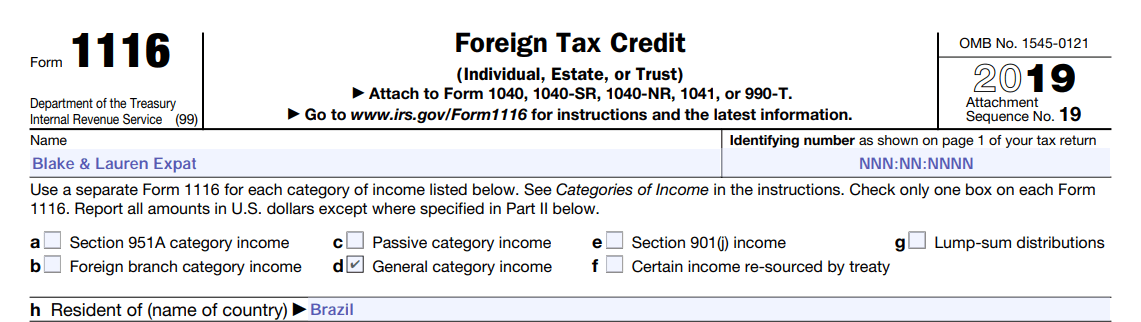

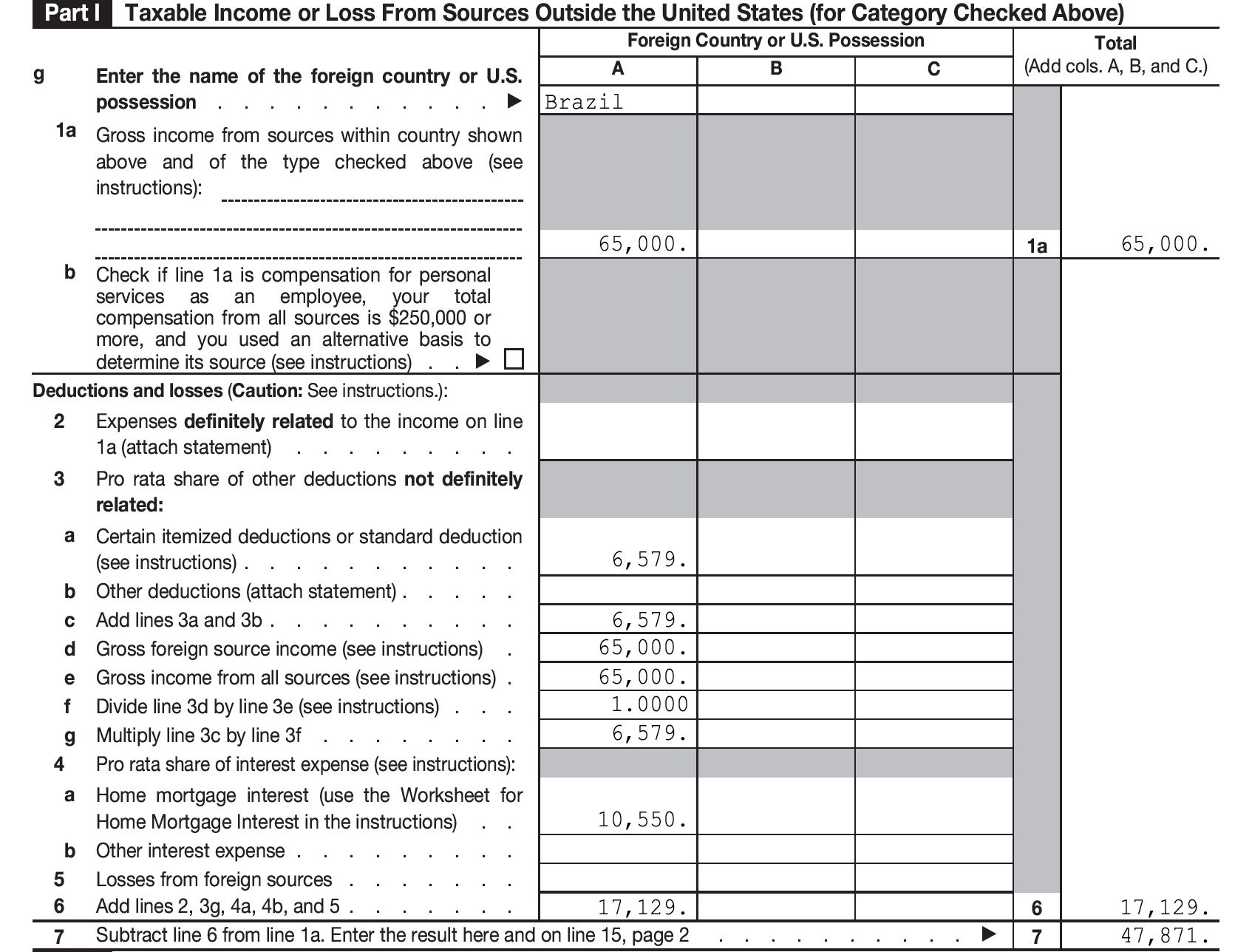

A Step By Step Guide To Form 1116 The Foreign Tax Credit For Expats

Source income as foreign source and the corporation elects to apply the treaty the income will be treated as foreign source.

901(j) income. However special rules in sections 901j and 952a5 generally deny foreign tax credits and impose other restrictions in the case of income attributable to countries with which the United States does not conduct diplomatic relations or which have been identified as sponsors of international. Wages salary and overseas allowances of an individual as an employee. Mason Department of Economics John Jay College-CUNY and The Roosevelt Institute March 2018 I thank David Alpert Heather Boushey Ba.

The payments referred to in paragraph 4 are payments which would be unlawful under the Foreign Corrupt Practices Act of 1977 if the payor were a United States person. A taxable income reduced by the amount of the net capital gain or B the amount of taxable income taxed at a rate below 28 percent plus 2 a tax of 28 percent of the amount of taxable income in excess of the amount determined under paragraph 1. IRC 901j denies the FTC for taxes paid to foreign countries with whom the United States has severed diplomatic relations see IRM 4611034.

Code 901 - Taxes of foreign countries and of possessions of United States. General category income may include. For federal income tax purposes A s income from the contract includes the amount of tax liability that is imposed by country X on A with respect to its income from the contract and that is assumed by country X.

While the Final Regulations significantly track to the Proposed Regulations and Temporary Regulations there are a few features to note. The regulations under section 704b providing coordination between 901m and the creditable foreign tax expenditure CFTE safe harbor rules were finalized without change. The term tested income group means an income group that consists of tested income within a.

1901-2 a 1 combines the statutory terms income war profits and excess profits tax into one concept. Select the Category of income CtrlT code 2 from the drop-down menu. General limited income is income that is not passive income Section 901 j income or income resourced by treaty or Lump-Sum distribution income.

Income tax for taxes paid to a foreign country. 90363 pages 901-906 DecemberHandle. 1901-2 a 1 ii.

901 Income Distribution Household Debt and Aggregate Demand. 901m which limits the creditability of foreign taxes in certain acquisition transactions where a taxpayer receives a basis step-up for US. What is Section 901 j Income Form 1116.

Income derived from each sanctioned country is subject to separate foreign tax credit limitations. The income is taxable. Determines that a waiver of the application of such paragraph is in the national interest of the United States and will expand trade and investment opportunities for United States companies in such country.

V Income subject to section 901j described in section 952a5. 901 j 5 A i. And for purposes of section 901 the amount of such.

A Critical Assessment J. If the taxpayer chooses to have the benefits of this subpart the tax imposed by this chapter shall subject to the limitation of section 904 be credited with the amounts provided in the applicable paragraph of subsection b plus in the case of a corporation. Passive Category Income- High Taxed.

Of an income tax in the US. If a sourcing rule in an applicable income tax treaty treats any US. Income from these countries is put in a separate category to prevent it from being offset by taxes paid to other countries.

Enter the Interest income in Banks SL etc. The income of such corporation derived from any foreign country during any period during which section 901j applies to such foreign country. A foreign assessment is an income tax if it has the predominant character.

A foreign tax credit FTC is generally offered by income tax systems that tax residents on worldwide income to mitigate the potential for double taxationThe credit may also be granted in those systems taxing residents on income that may have been taxed in another jurisdiction. Therefore you must file. No credit is allowed for foreign taxes imposed by and paid or accrued to certain sanctioned countries.

The taxes paid are permanently disallowed. Certain Income Re-sourced by Treaty. Restrictions under section 901.

Income Re-Sourced by Treaty. Tax purposes but no corresponding basis step-up for foreign tax purposes. Section 901 generally allows taxpayers a credit against US.

Go to Screen 11 Interest Income. Enter the Name of Payer code 800. The payments referred to in paragraph 4 are payments which would be unlawful under the Foreign Corrupt Practices Act of 1977 if the payor were a United States person.

Section 901j1A denies the credit for taxes paid or accrued or deemed paid or accrued under sections 902 or 960 to any country described in section 901j2A if the taxes are with respect to income. As described above the Final Regulations. Section 901j1 imposes restrictions in the case of income and taxes attributable to certain countries.

111-226 enacting new Sec. In 2010 President Barack Obama signed PL. A credit is not allowed for paidaccrued taxes that are imposed by certain sanctioned countries.

These wages cannot be excluded from income using the Foreign Earned Income Exclusion. Subpart F Income Defined. Foreign Income Taxpayers.

901 j 5 A ii. The credit generally applies only to taxes of a nature similar to the tax being reduced by the credit taxes based. Publication 901 will tell you whether a tax treaty between the United States and a particular country offers a reduced rate of or possibly a complete exemption from US.

Income tax for residents of that particular country. Hutton J P Lambert P J 1980. Foreign income is reported in one of six categories with an appropriate code 951A RBT income re-source by treaty 901j income earned from a sanctioned country FB QBUs in addition to the more familiar passive and general income categories.

However a foreign tax credit may be claimed for foreign taxes paid or accrued with respect to section 901j income if such tax is paid or accrued to a. More In Forms and Instructions. The income of such corporation derived from any foreign country during any period during which section 901 j applies to such foreign country.

Section 901j income is income earned from a sanctioned country.

2

Characteristics Of Studied Low And Middle Income Countries By Who Download Scientific Diagram

Pdf Managing Tourism As A Source Of Revenue And Foreign Direct Investment Inflow In A Developing Country The Jordanian Experience

2

2

2

A Step By Step Guide To Form 1116 The Foreign Tax Credit For Expats

A Step By Step Guide To Form 1116 The Foreign Tax Credit For Expats

Instructions For Form 5471 01 2021 Internal Revenue Service

Figure A2 Cardiac Surgical Safety Checklist Download Scientific Diagram

Pdf Protective Factors And The Development Of Resilience In The Context Of Neighborhood Disadvantage

Pdf The Income Pollution Relationship And The Role Of Income Distribution Evidence From Swedish Household Data

2

2

Income){kind=link}

Posting Komentar untuk "901(j) Income"