6 Income Under 44ad

In the case of such assessees the presumptive income under section 44ADA would be a sum equal to 50 of the total gross receipts or a higher amount as may be provided for by the assessee. Now come to an interesting aspect.

Section 44ad Income Tax Presumptive Income Scheme Of Business

Section 44AD overrides the chapter of PGBP.

6 income under 44ad. Section 44AD the provisions of section 44AA relating to maintenance of books of account will not apply. Fill ITR 4 under section 44ad. Amount of Gross Turnover received in cash Deemed Profit Gain - 8 2.

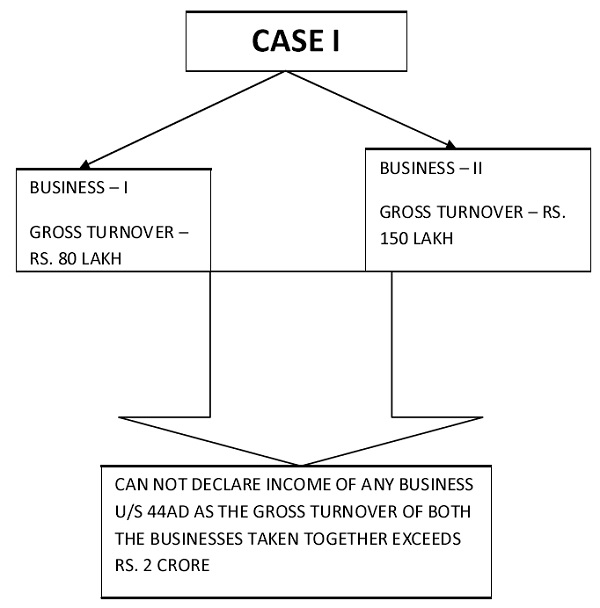

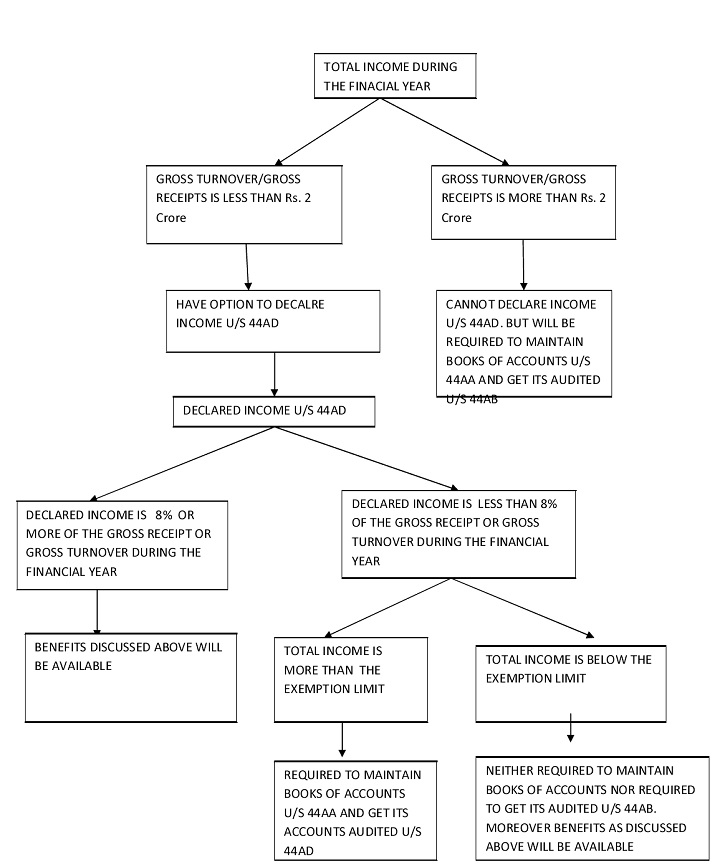

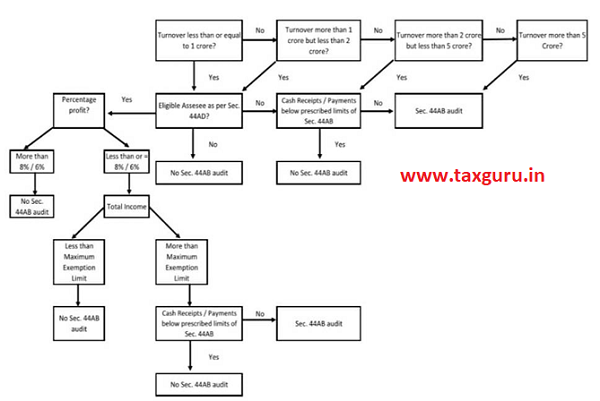

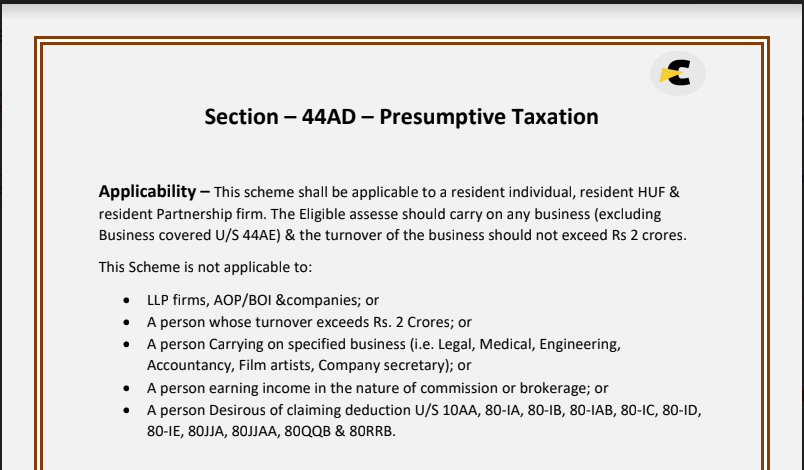

If an assessee is declaring his income as per section 44AD the requirement relating to maintenance of books of accounts and audit of books of account is not applied. But Losses are dealt in accordance with Chapter VI which consists of section 70-80. The gross sales or turnover of the business should be less than or equal to INR 2 Crore.

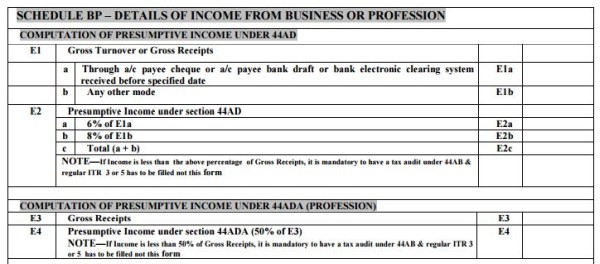

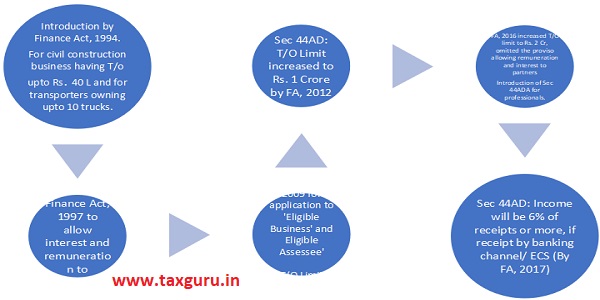

As per the provisions under Section 44AD computed presumptive income taking 6 or 8 of gross receipts or turnover of the eligible business for the previous year. In order to achieve the Governments mission of moving towards a less cash economy and to incentivise small traders businesses to proactively accept payments by digital means it has been decided to reduce the existing rate of deemed profit of 8 under section 44AD of the Act to 6 in respect of the amount of total turnover or gross receipts. Note- For Amt received directly in bank we have to take 6 as Profit instead of 8 Note- 86 is Minimum Profit to be shown Assesses can show more than 8 profit also What if assess show less than 86 profit or loss.

The rate under sec 44AD would be prescribed as 8 of total turnover or gross receipts. If their turnover is below the limit of Rs. If your actual profit is less than 6 of turnover theres no way to show lower than 6 as profit without getting a tax audit done.

It is not allowed as per Section 44AD He has to compulsorily gets accounts audited and pay tax on it. Under section 44AD The presumed income of the assessee is deemed to be 8 of the gross turnover for the financial year however the assessee can claim a higher profit. However the person can claim deduction available under chapter VI-A from presumptive income.

As per the provisions under Section 44AD computed presumptive income 6 or 8 of gross receipts or turnover of the eligible business for the previous year is considered as the net income for the business covered under the presumptive taxation scheme. It comes under Section 44AD Services covered under section 44ADA as follows. 2 Cr as per section 44AB applicable for compulsory tax audit and.

Now this is where it becomes dicey. To opt for Presumptive Taxation Scheme under Section 44AD the following two conditions should be satisfied. In order to promote digital transactions and to encourage small unorganized business to accept digital payments it is proposed to amend section 44AD of the Act to reduce the existing rate of deemed total income of eight per cent.

Section 44AD is applicable if the turnover is not exceeding Rs. From Financial year 2017-18 6 is taken in lieu of 8 in respect of the amount of. Then the audit would not be compulsory.

Provisions under section 44AD. If you opt for 44 AD in year 2019-20 you have to continue showing under 44AD scheme for years 2020-21 2022-23 2023-24 and 2024-25. To six per cent in respect of the amount of such total turnover or gross receipts received by an account payee cheque or account payee bank draft or use of electronic.

Amount of Gross Turnover received by an account payee cheque or an account payee bank draft or use of electronic clearing system through a bank account Deemed Profit. The presumptive income computed under section 44AD is treated as net income for the business and no further deduction is allowed under section 30 to 38 of the Income-tax Act 1961. If eligible assessee received any turnovergross receipts by way of any digital mode he can claim 6 in lieu of 8.

Income from business of plying hiring or leasing goods carriages Section 44AE of Income Tax 1961. No the only disadvantage of 44AD is that you have to show your profit more than 8 or 6 whichever applicable for 5 continuous years. Maintaining books of accounts are not mandatory.

In other words if a person adopts the provisions of section 44AD and declares income 6 or 8 as the case may be of the turnover then he is not required to maintain the books. However the assessee can claim higher profits. 1 Cr not Rs.

Before amendment done by Finance Act 2017 in section 44AD the Presumptive Income to be 8 which will be amended to 6 in respect of the amount of such total turnover or gross receipts received by an account payee cheque or account payee bank draft or use of electronic clearing system through a bank account during the previous year or. The taxpayer should report 68 or more of the gross sales or turnover as income in the ITR. Who are offering income for taxation at less than 8 or 6.

2 Cr subject to the conditions that such assessee offers minimum of 8 or 6 of the turnover as income. Calculation of Presumptive Income under Section 44AD 1. Income from other head of income like Capital Gains House Property shall be calculated normally are not subject to limit of 8 or 6 as the case may be.

Calculation of Presumptive Income under Section 44AD. Yes if assessee opted for presumptive taxation as per section 44AD they can show 8 or 6 income as the case may beNon- Audit Case. In case an eligible assessee carrying on the eligible business the profits and gains of such business is deemed to be 8 of the total turnover or gross receipts from such business.

Any deductions which are allowed under section 30 to 38. First up its important to note that futures and options FO transactions are treated as business income under the Income tax act. Although Government has introduced the presumptive rate of 6 to motivate the payment digitally.

6 in the case of digital receipts or 8 is the minimum net income is considered as the taxable limit. No audit of the books is required. In short now there are three limits of turnover for tax audit us 44AB for tax audit.

Interesting Issues Under Section 44ad 44ada And 44ae Of

Itr Form To Be Filled For Small Proprietorhip Covered In 44ad 44ae

Bank Channel Other Mode Under 44ad Income Tax Tax Queries

Section 44ad Of Income Tax Act 1961 After Budget 2016

Section 44ad Presumptive Income Under Income Tax Act

Section 44ad Of Income Tax Act 1961 After Budget 2016

Can A Person Use Section 44ad And Section 44ada Of Income Tax Act

Interesting Issues Under Section 44ad 44ada And 44ae

Tax Audit For A Y 2020 21 U S 44ab Vis A Vis 44ad 44ada

Section 44ad Of Income Tax Act 1961 After Budget 2016

8 6 Scheme For Small Business For Section 44ad Small Proprietorshi

Tax Audit Under Section 44ab V S Section 44ad

Section 44ad Presumptive Taxation For Small Businesses

Section 44ad Of Income Tax Act For Ay 2019 20 Eligibility Applicability

{kind=link}

Posting Komentar untuk "6 Income Under 44ad"