Income Under Subpart F

952a4 must match the amounts disclosed as illegal payments made by the companys CFCs to foreign officials or governments. If 70 of gross income is Subpart F i th ll f th CFC i iincome then all of the CFCs gross income is considered Subpart F income 26.

Attend This Webinar To Refresh Your Understanding Of Subpart F Income And Avoid Common Errors And Mistakes In Completi Money Budgeting Money Ways To Save Money

The amounts classified as Subpart F income because of Sec.

Income under subpart f. Taxation if the foreign corpora-tion was not a CFC for an uninterrupted period of at least 30 days. When a CFC has Subpart F income under IRC Section 952 that means the US. For example if a CFC was formed during the last month of its taxable year any Subpart F income earned during that short year would not be taxable un-der Subpart F.

For purposes of this subpart the term subpart F income means in the case of any controlled foreign corporation the sum of. Foreign base company income under 954. On December 7 2011 The US.

Certain insurance income under 953. Residents gross income that were required under the Subpart F provisions with respect to their controlled foreign. Subpart F refers to foreign income and Subpart F income is codified in Internal Revenue Code section 952.

For purposes of this subpart the term subpart F income means in the case of any controlled foreign corporation the sum of. There are two major exceptions to deferral of income earned by foreign subsidiaries the Subpart F and the Passive Foreign Investment Company PFIC regimes. 14 An exception to FBCI arises where a CFCs income was subject to an effective rate of income tax imposed.

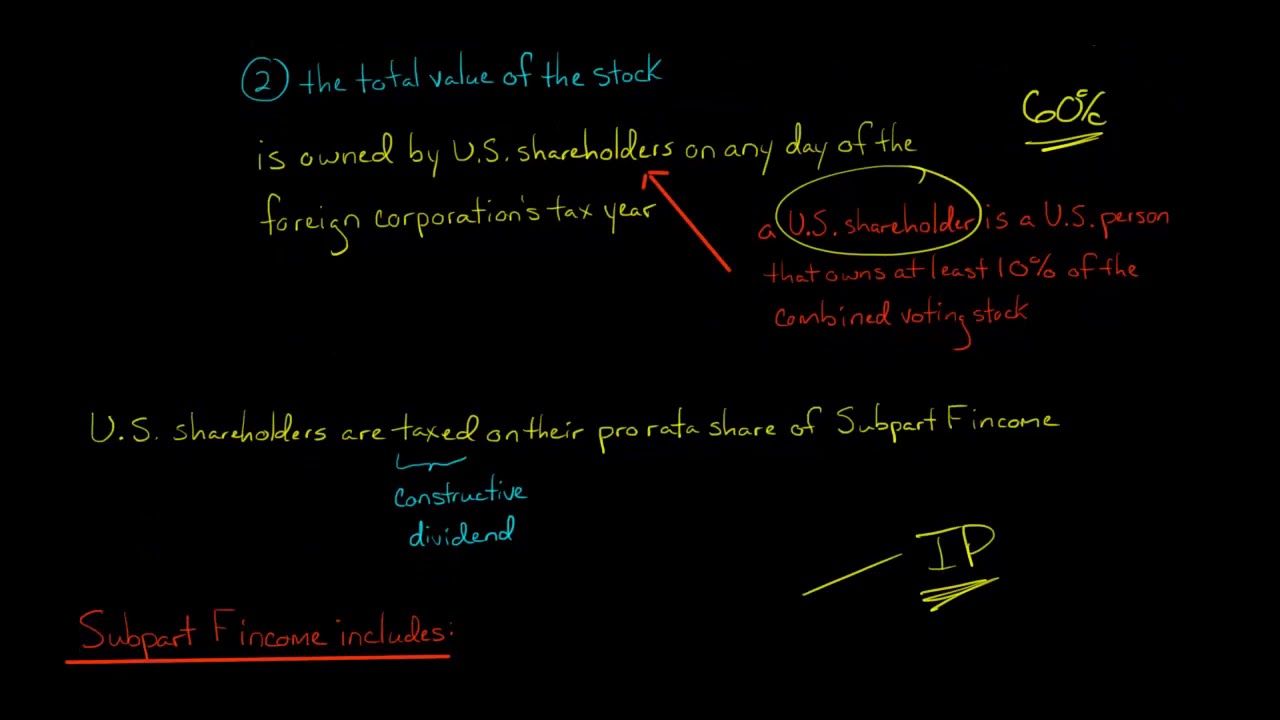

Under Subpart F certain types of income and investments of earnings of a foreign corporation controlled by US shareholders controlled foreign corporation or CFC are deemed distributed to the. 952 a 1. Subpart F income is Foreign Base Company Income FBCI as defined under IRC.

Section 951A does not have an independent high-tax exception for items of CFC income that would not otherwise qualify under Subpart F. Any dividend received which is considered paid from amounts previously taxed under Subpart F. Under Subpart F rules a parent corporation nets income at the entity level meaning the taxable income from each CFC is attributed to the parent.

For a C corporation Subpart F income is subject to a maximum tax rate of 21 percent and for individuals and pass-through entities the maximum income tax rate is 37 percent regulations also apply the 38 percent net investment income tax under certain circumstances to income of and distributions from CFCs but that tax is not addressed. If Subpart F income is less than the lesser ofIf Subpart F income is less than the lesser of. 952 a In general.

Shareholders may have to pay tax on the earnings. Subpart F Income is taxed at ordinary tax rates not at the lower dividend or capital gain rate. In general it consists of movable income.

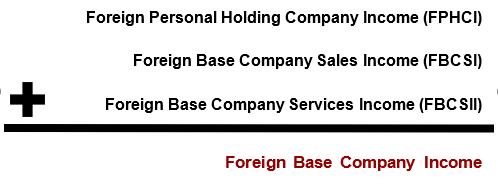

952 a 2. The GILTI regime excludes inclusions under Subpart F or items of CFC income that would be included under Subpart F but for the high-tax exception from tested income used to determine the GILTI inclusion. Subpart F income includes a CFCs foreign base company income FBCI13 which is the sum of its FPHCI foreign base company sales income and foreign base company services income.

Related-party services income under Subpart F is any income whether in the form of compensation commissions fees or otherwise derived in connection with the performance of technical managerial engineering architectural scientific skilled industrial commercial or like services that are performed for or on behalf of a related person and that are performed outside the CFCs country of. 954a which includes foreign personal holding company income or FPHCI which consists of investment income such as dividends interest rents and royalties. De minimis amounts of Subpart F income in absence of other Subpart F income in the period.

Both of these regimes constitute traps for the unwary who may unknowingly be subject to taxes and penalties for failure to comply. Another category of Subpart F income is Foreign Base Company Sales Income which. Therefore efforts to mitigate the Subpart F pickup for example through bifurcation discussed below must be considered at the time of the negotiation of the NPA not after its execution.

952 of the Code defines Subpart F income to include the following items. Other sections of the Code then further categorize these items as well as provide exceptions to such categories and. Subpart F income does not include any item includible in the CFCs gross income as income from sources within the United States that is effectively connected with the conduct by the CFC of a trade or business in the US unless the income is exempt from tax or subject to a reduced rate of tax pursuant to a treaty obligation of the US.

Essentially Subpart F Income involves CFCs Controlled Foreign Corporations that accumulate certain specific types of income primarily passive income. Subpart F Income Defined. 5 of the gross income or 1 000 0001000000 then Subpart F income deemed to be zero.

Tax Court ruled that inclusions in US. Under prior law Subpart F income earned by a CFC was not subject to US. 952 a In General.

Insurance income foreign base company income FBCI international boycott factor income illegal bribes and kickbacks and income derived from certain designated terrorism-sponsoring countries. Insurance income as defined under section 953 IRC. Illegal bribes kickbacks or other illegal payments made by the CFC.

Such income if the CFC has a deficit in EP in which case it is deferred from recognition until the CFC has positive EP. Subpart F income includes Foreign Base Company Services Income which is income received by a CFC from the performance of services for or on behalf of a related person. Subpart F income includes subject to certain limitations.

There are many categories of Subpart F income.

Subpart F Income Of Controlled Foreign Corporations

International Tax Blog 951 Subpart F Income

Subpart F Income How Is It Taxed In The U S New 2021

The Irs Announced That It Is Lowering From 85 To 80 The Amount Taxpayers Are Required To Have Paid In Order To Escape An Un Tax Refund Irs Federal Income Tax

Digging Deeper Into Subpart F Income Asena Advisors

Subpart F Income Partnership Blocker Update International Tax Blog

1 951 1 B 2 Example 4 Subpart F Income Hopscotch Rule Youtube

Subpart F Income Of Controlled Foreign Corporations U S Taxation Youtube

Subpart F Generally Foreign Personal Holding Company Income University Of Cincinnati Lindner College Of Business

Pin On Law Tax Business

What Is Irs Subpart F How Has Tax Reform Changed It

Subpart F Income Of Controlled Foreign Corporations

2

2

{kind=link}

Posting Komentar untuk "Income Under Subpart F"