Income U/s 44ae

TAX INFORMATION AND SERVICES. In case vehicle is used for part of month kindly select complete month ie.

Presumptive Income Itr4 Schedule Bp Goods Section 44ae

Other than heavy goods vehicle Income per month per vehicle ie.

Income u/s 44ae. Section 44AE of The Income Tax Act 1961. Where us 44AA or 44AD or 44ADA it is mentioned that books of accounts are not required to be maintained by those disclosing income us 44AD 6 or 8 or 44ADA 50. Can department ask for details of bank and cash receipt payment during the year relating to business.

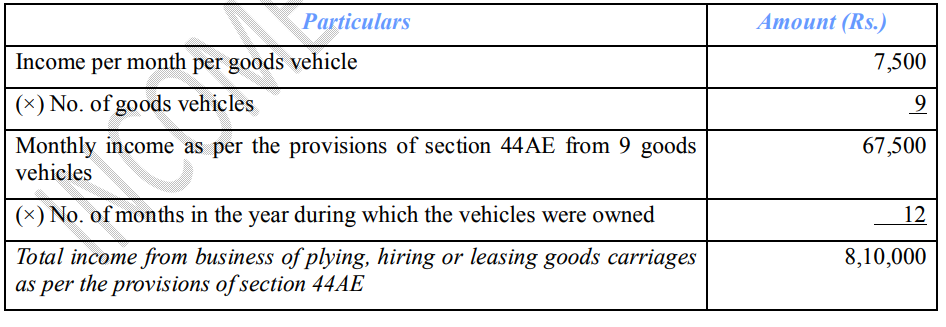

1 month 1 day should be treated as 2 months. For example if you are engaged in the business of plying hiring or leasing of goods carriage and you own 7 vehicles throughout the year then your income us 44AE shall amount to Rs. Any individual paying salary of Rs.

7500 x 7 vehicles x 12 months. Professionals with income from profession listed US 44AA1 in the fields of medical legal architectural engineering technical consultancy accountancy interior decoration film artists information technology professionals company secretary and the business of being an. The Total amount carry forwarded to E5 Presumptive Income from goods carriage under section 44AE.

Therefore assessee declaring income us 44AD 44ADA or 44AE is liable to deduct TDS. As per Section 44AE eligible assesse has to declare Rs. Other than heavy goods vehicle 4500 No.

Would be required to deduct TDS even though he is declaring income us 44AD. Income from other goods vehicle ie. 7500 per month or part thereof during which the goods vehicle other than heavy goods vehicle is owned by the assessee during the previous year.

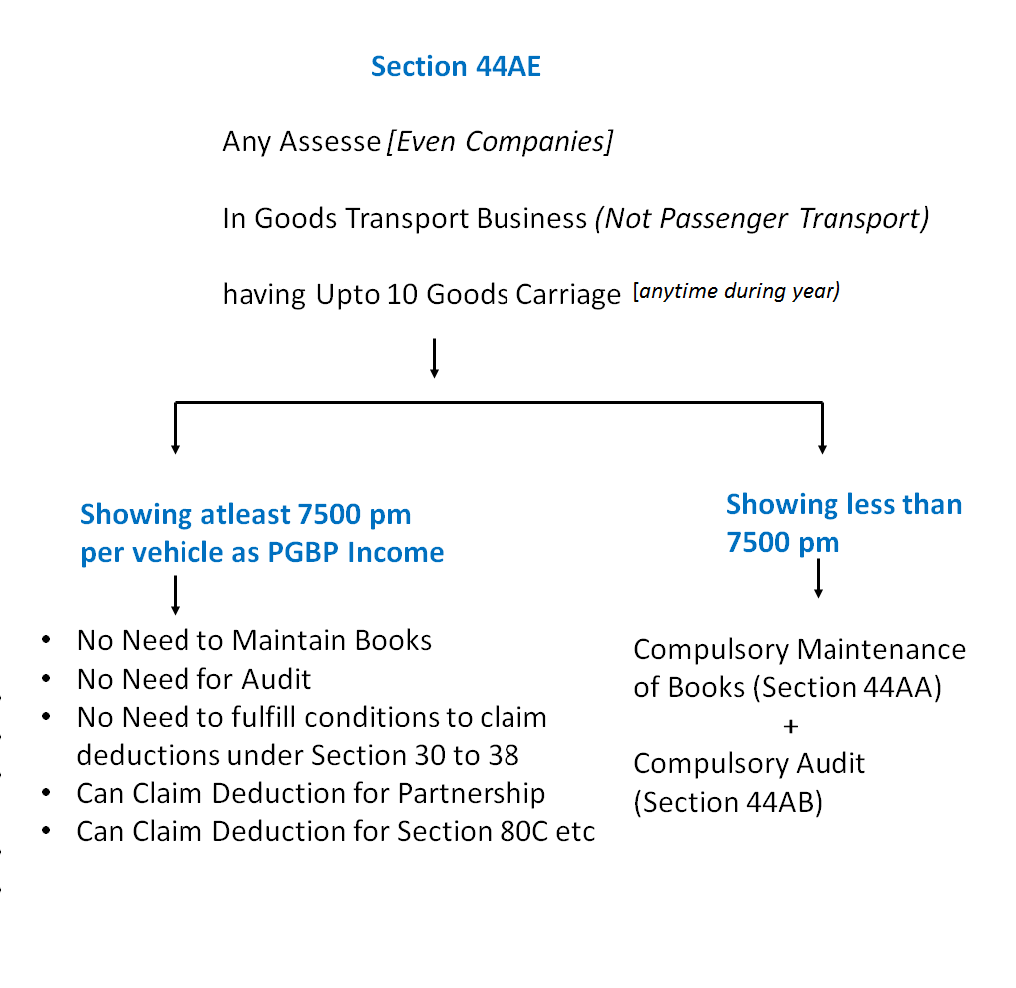

Notwithstanding anything contained in the foregoing an assessee who claims that his profits and gains from the profession are lower than the profits and gains specified in sub-section 1 and whose total income exceeds the maximum amount which is not chargeable to income-tax shall be required to keep and maintain such books of account and other documents as required under sub. This section applies specifically on assessees carrying on business of plying hiring or leasing good carriages. Every person is required to deduct TDS us 192 if the estimated salary exceeds the maximum amount not chargeable to tax.

5000 per month assessee is not permitted to claim any deduction under sections 30 to 38 including depreciation or unabsorbed depreciation. 1000 per ton in case of heavy goods carriage per month as his income for availing the benefit of Section 44AE ie. The aim is to simplify the taxation compliances provide relief from the tedious job of maintaining books of accounts and provide a standard income calculation approach.

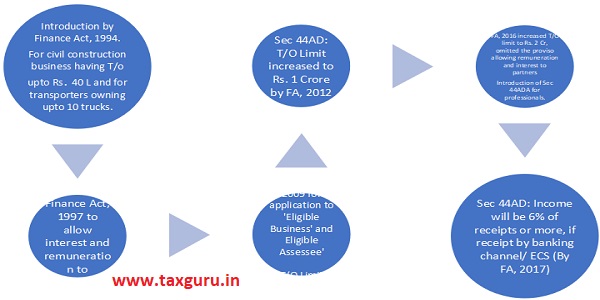

A for sub-section 2 the following sub-section shall be substituted namely. The presumptive taxation scheme us 44AE of Income Tax Act can be adopted by. Amendment of section 44AE.

Any class of taxpayer ie. Advance Tax Section E8 Finally provided you the Total Income chargeable under business us 44AD 44ADA 44AE. Individual HUF Partnership Firm LLP Company Who are not eligible for presumptive taxation scheme us 44AE.

The person who is earning income in the nature of commission or brokerage. Section 44AE inter alia provides that the profits and gains shall be deemed to be an amount equal to seven thousand five hundred rupees per month or part of a month for each goods carriage or the amount claimed to be actually earned by the assessee whichever is higher. Turnover is 45 Lacs Expenditure as per Sec 30-38 is 41 Lacs.

Businesses have more than 10 good carriages. Total presumptive income us 44AE. The current presumptive income scheme is applicable uniformly to all classes of goods carriages irrespective of their tonnage capacity.

As per the provisions of section 44AE in respect of goods vehicle other than heavy goods vehicle income will be computed Rs. Section 44AE of the income tax act 1961 is an income scheme introduced by the Income Tax Department for small and medium enterprises. The business of hiring plying leasing of goods carriage US 44AE.

As per the Income-tax Act a person engaged in business or profession is required to maintain regular books of account and further he has to get his accounts audited. Income as per Sec 44AE 360000. In India Income Tax is the self-assessed tax that is an assessee calculates his taxes on his own and discloses it to the government in an income tax return.

Business of plying hiring or leasing of goods carriages referred to in section 44AE. Special provision for computing profits and gains of business of plying hiring or leasing goods carriages. Presumptive income under section 44AE in case of goods carriage.

Person who is carrying on any agency business. Income is 4 lacs. In section 44AE of the Income-tax Act with effect from the 1st day of April 2019.

S ection 44AE inter alia provides that the profits and gains shall be deemed to be an amount equal to 7500- per month or part of a month for each goods carriage or the amount claimed to be actually earned by the assessee whichever is higher. A person who is engaged in any profession as prescribed us. For heavy goods vehicleincome shall be an amount equal to Rs1000- per ton of gross vehicle weight or unladen weight as the case may befor every month or part of a month during which the heavy goods vehicle is owned by the assessee in the previous year or an amount claimed to have been.

For instance if you have 5 vehicles engaged in the business of plying hiring or leasing of goods carriage during the financial year 2018-19 then your estimated income under section 44AE. Minimum Income to be offered for taxation us 44AE. This section states that if an assessee is carrying on the above mentioned business.

Thus in this case the assessee may opt out and declare income of 4 lacs it will not be covered by Sec 44AA Sec 44AB. In such a case the income will be computed as per rules given us 28 44. As per the provisions of section 44AE from the net income computed at the prescribed rate ie Rs.

To give relief to small taxpayers from this tedious work the Income-tax Act has framed the presumptive taxation scheme under sections 44AD 44ADA and 44AE. Total income as per the provisions of sections 44AE from 5 heavy goods vehicleA 300000. 2 For the purposes of sub-section 1 the profits and gains from each goods carriage.

Income from business of plying hiring or leasing goods carriages Section 44AE of Income Tax 1961 Section 44AE. Profit as per Sec.

How To Calculate Presumptive Income Under Section 44ae

Section 44ae Presumptive Income Of Goods Transport Business

Presumptive Taxation U S 44ae For Goods Ca Sparks Associates Chartered Accountants

44ae Income Tax Tax Heal

Interesting Issues Under Section 44ad 44ada And 44ae

Presumptive Taxation Scheme U S 44ad 44ada 44ae Rja

Section 44ae Presumtive Taxation Scheme Caxpert

Goods Carriage Business Go With Section 44ae No Books No Audit

Section 44ae Limit Changed For Large Motor Vehicles Budget Changes 2

Section 44ae Of Income Tax Act Presumptive Taxation For Transporters

How To Calculate Presumptive Income Under Section 44ae

How To File Income Tax Return Itr 4 U S 44ae Ay 2020 21 For Transport Business Itr 4 Youtube

S 44ae Presumptive Profit For Transporter Ay2019 20 Itr 4 Income Tax Finance Gyan Youtube

![]()

Section 44ae Presumptive Income Provisions For Transporters

{kind=link}

Posting Komentar untuk "Income U/s 44ae"